🧑💻 Developer-First #174 - From ROI to RIFs: How the AI era is reshaping enterprise strategy

As AI delivers real ROI, hiring slows and budgets shift toward internal R&D, fuelling a new boom in DevTools and Software Infrastructure.

Hello friend,

Last week, two headlines captured the paradox of the AI era.

On one side, Wharton’s 2025 AI Adoption Report is showing that 75% of large enterprises now report a positive ROI from AI, a sharp reversal from the “95% of pilots fail” narrative just a year ago. Companies aren’t just experimenting anymore; they’re scaling, measuring, and reorganising around AI productivity.

On the other side, Amazon announced up to 30,000 corporate layoffs, calling it a “cultural reset,” not an AI-driven move. But the timing is no coincidence. As AI efficiency compounds, the next corporate cycle is clear: fewer hires, leaner teams, and more capital redirected into automation and internal tooling.

Most enterprises won’t spend their savings on headcount. They’ll spend it on leverage. According to the same Wharton study, 30% of AI budgets in 2026 will go to internal R&D, a sign that companies are turning inward to build the infrastructure, platforms, and developer tools that drive measurable gains.

That’s why I’m more bullish than ever on DevTools and Software Infrastructure. As enterprises freeze hiring but double down on engineering leverage, the next wave of value creation won’t come from adding people. It’ll come from building the systems that make smaller teams exponentially more productive.

P.S. If you’re a CTO, VP Engineering, or technical executive, you should join the Unicorn CTO community, a free network of 1,000+ European tech leaders who learn and connect with peers. You’ll get access to exclusive events and a private Slack group where the top engineering leaders in Europe exchange strategies every week.

Deal of the Week — Applied Compute raises $80M to build “Specific Intelligence”

Applied Compute just came out of stealth with an $80 million seed round from Benchmark, Sequoia, Lux, Elad Gil, and others. Founded by three former OpenAI researchers, the company is targeting enterprises that want to move beyond general-purpose AI and build in-house agent workforces trained on their proprietary data and workflows.

Their thesis (what they call Specific Intelligence) is that the next edge won’t come from using the same GPT models as everyone else, but from owning and operating custom agents that reflect how a company actually works. Early customers like are already using Applied Compute’s stack to train and deploy specialised models that achieve state-of-the-art results on internal benchmarks.

💭 My take: with 30% of GenAI budgets now dedicated to internal R&D, like building proprietary models, enterprise AI will be about ownership, control and embedded expertise. Read more about this deal here. Also, you’ll find all the other transactions from last week in The Changelog at the end of this newsletter.

AI adoption in enterprises - From pilots to performance

According to the 2025 Wharton–GBK AI Adoption Report, 75% of large enterprises now report a positive ROI from AI. A stunning reversal from the “95% of pilots fail” narrative of just a year ago. The study calls this new phase accountable acceleration: AI is no longer experimental, it’s operational. 82% of enterprise leaders now use GenAI weekly, nearly half daily, and 72% formally measure ROI, tying investment directly to productivity and profitability.

Even more telling, 88% plan to increase budgets in 2026, with 30% of total tech spend now flowing into internal AI R&D. AI ownership has also moved to the C-suite: 67% of enterprises have executive-level accountability and 60% already employ a Chief AI Officer. The signal is clear: we’ve entered the AI deployment era, where the winners aren’t those experimenting fastest, but those executing best.

Revenue Intelligence for DevTools and Infra startups

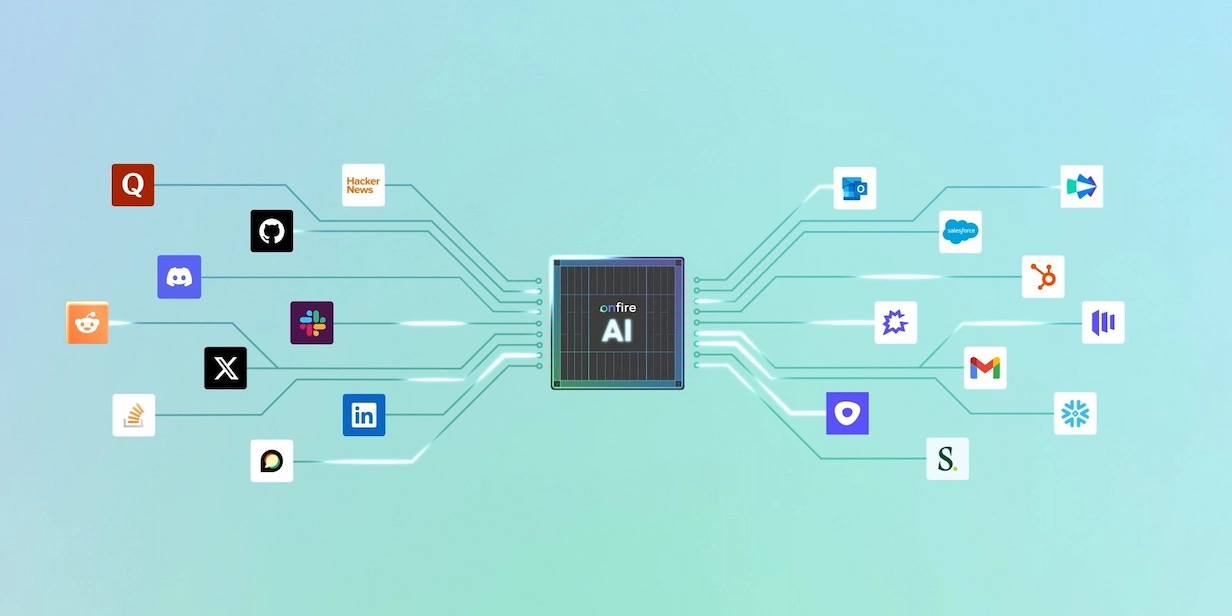

With Onfire’s $20M launch last week, and Reo.Dev’s $4M seed announced early October, a new GTM category is emerging: Revenue Intelligence built for DevTools and software infrastructure. As you know, selling to technical buyers is nothing like a typical SaaS playbook (I know a thing or two about that). Traditional CRM and intent tools can’t see where developers actually make decisions: GitHub commits, package installs, Docker pulls, or open-source discussions.

That’s the gap Onfire, Reo.Dev and similar tools are closing. Both use vertical AI and proprietary developer data to surface real buying intent and link bottom-up adoption to top-down enterprise deals. If you’re selling to CTOs, stop tracking activity and start mapping intent. The teams who understand developer signals will own the next wave of GTM efficiency in infrastructure and DevTools.

The Changelog - Week of October 27th, 2025

Last week, 11 companies raised $550 million across 9 product categories in 3 countries. Europe-based companies attracted 2% of the total funding vs 93% for North America-based companies and another 6% for Asia-based companies (incl. Israel). Two of these companies distribute or contribute to an open-source project. On the M&A side, no companies were acquired.

Funding Rounds

Fireworks AI, from Redwood City 🇺🇸 raised $250 million in Series C funding co-led by Lightspeed Venture Partners, Index Ventures, and Evantic. Fireworks AI provides a generative AI platform-as-a-service with the fastest inference engine to build production-ready, compound AI systems. (more)

Cartesia, from San Francisco 🇺🇸 raised $100 million in Series B funding from Kleiner Perkins, Index Ventures, Lightspeed, and NVIDIA. Cartesia is developing the next generation of AI — ubiquitous, interactive intelligence that can run anywhere. (more)

Applied Compute, from San Francisco 🇺🇸 raised $80 million in Seed funding Benchmark, Sequoia, Lux, Elad Gil, and others. Applied Compute builds “Specific Intelligence” for enterprises, enabling them to train custom models and deploy in-house AI agent workforces. (more)

CoreStory, from Berkeley 🇺🇸 raised $32 million in Series A funding led by Tribeca Venture Partners, NEA, and SineWave Ventures. CoreStory delivers enterprise-grade code intelligence for software modernisation, governance, and onboarding, improving tools like GitHub Copilot through deep structural analysis. (more)

Mem0, from San Francisco 🇺🇸 raised $24 million in Series A funding led by Basis Set Ventures. Mem0 provides the memory layer for personalised AI, enabling context persistence across AI applications. (more)

Onfire AI, from Tel Aviv 🇮🇱 raised $20 million in Series A funding led by Grove Ventures and TLV Partners. Onfire AI is the revenue intelligence platform for software infrastructure companies, using AI to find and reach technical buyers with real-time intent data. (more)

Impala AI, from Tel Aviv 🇮🇱 raised $11 million in Seed funding led by Viola Ventures and NFX. Impala AI is building a scalable, affordable, and controllable AI stack for large language model inference. (more)

CUE Labs, from Zug 🇨🇭 raised $10 million in Seed funding led by Sequoia Capital and OSS Capital. CUE Labs unifies configuration management across complex systems, helping teams eliminate configuration chaos and ensure software consistency. (more)

Polygraf AI, from Austin 🇺🇸 raised $9.5 million in Seed funding led by Allegis Capital. Polygraf AI builds AI-native security solutions to detect fraud, data leaks, and compliance risks in enterprise environments. (more)

Wild Moose, from San Francisco 🇺🇸 raised $7 million in Seed funding led by iAngels. Wild Moose helps on-call developers identify the root cause of production incidents faster through a conversational AI trained on their environment. (more)

TestSprite, from Seattle 🇺🇸 raised $6.7 million in Seed funding led by Trilogy Equity Partners. TestSprite provides a testing platform that accelerates release cycles and improves software quality, offering 10x faster testing across systems. (more)